Rethinking Co-Creation in the Sports Industry

Pillar of Growth Strategy: Is the "15 Trillion Yen Sports Industry Market" Just a Dream?

The aim is to expand the market size of the sports industry from 5.5 trillion yen in 2012 to 15 trillion yen by 2025. This is one of the major goals of Japan's growth strategy.

Whether one views this number as large or small is a matter of personal perspective. However, it is difficult to label this as an entirely reckless plan. In fact, it might even be considered a modest goal. The basis for this assessment lies in how the target was calculated.

In 2012, the base year for setting the target, Japan's market size was 5.5 trillion yen, while the US market size was over 50 trillion yen. Despite the fact that Japan's population is about half that of the US and its GDP is about a third, the disparity in sports market size is a staggering tenfold. Of course, due to geographical and cultural differences, a simple equivalence is not feasible. However, it is clear that setting such a target is not excessively unrealistic.

Nonetheless, the current environment surrounding the sports market is not necessarily favorable. With the exception of some professional leagues, such as the Nippon Professional Baseball (NPB) and the J-League, most organizations are not performing well. The reality is that most sports organizations and individuals have not succeeded in monetizing core sports assets, such as games and players. Compounding this issue are difficult business conditions due to social trends such as a declining birthrate and aging population, as well as the impact of the COVID-19 pandemic.

For example, let’s examine the results of the "2021 Sports Marketing Basic Survey," a joint survey by Mitsubishi UFJ Research & Consulting and Macromill. This survey estimates the size of the sports participation market, which includes core markets for sports activities (stadium spectator market + sports goods purchase market + sports facility usage/membership market). Note that this market does not include advertising, promotion, or sports lotteries, which are not essential for sports activities. The size of the sports participation market in 2021 was approximately 1.1 trillion yen, representing a 32.0% decrease from 2020 and was less than half of the pre-COVID-19 pandemic size.

As new lifestyles are beginning to take hold amid the COVID-19 pandemic, everyday sports activities such as exercising and watching games are gradually returning to normal. However, irreversible changes are occurring that prevent a complete return to pre-pandemic conditions. These changes include positive developments such as the rise of on-demand streaming and home viewing of sports, but they also challenge the traditional analog and in-person approach to sports.

It is not just the sports themselves that need to be examined. In today's world, where popular entertainment is diversifying, attracting customers and monetizing sports is not easy unless you have a very popular sport, a strong team, or top athletes. The American platform Netflix has aptly stated, "The real competitor we need to compete with is not other video streaming services, but Disneyland." To put it bluntly, for today’s consumers who enjoy a wide range of popular entertainment options, sports are just one of many choices.

A shortage of "management talent" has long been seen as one of the factors impeding the growth of the domestic sports industry. The Sports Agency has also pointed out that there is a limit to the number of people with specialized knowledge, experience, and skills in areas such as finance and marketing who can manage profitable businesses. (For example, see the Sports Agency’s publication "Current Situation and Issues in the Development and Utilization of Sports Management Talent" (October 2016).)

Still, there are no signs that the Japanese government is looking to alter the growth goals of the sports industry. On the contrary, the Sports Agency’s "Sports Open Innovation Promotion Project" is intensifying its support through initiatives such as hosting contests using sports tech and developing industry-specific platforms. What does this indicate? At a glance, is there a game-changing strategy that could turn the 15 trillion yen market, which seems like a distant dream, into reality?

Here, let us revisit what the sports industry is, its definition, how to understand market size, and consider whether there is a winning strategy for achieving our goals.

The Path to Growth Industry with Government Focus: Integration with Other Industries

When you hear the term "sports industry," what industries, companies, and businesses come to mind? Unlike finance or manufacturing, the sports industry does not have a clear classification and exists across many sectors.

Traditionally, the structure of the sports industry in Japan was defined primarily around human activities such as "playing," "watching," and "supporting" sports. In that scheme, the following sports activities or goods and services were the main components of the sports industry.

・Professional sports: professional baseball, J-League, etc.

・Sporting events: Olympics, World Cup, etc.

・Sports information: Distributed by media such as television stations and newspapers

・Manufacturers/stores: dealing in sporting goods

・Sports facilities: gyms, fitness centers, etc.

・Sports promotion: Regional development by government and public institutions, etc.

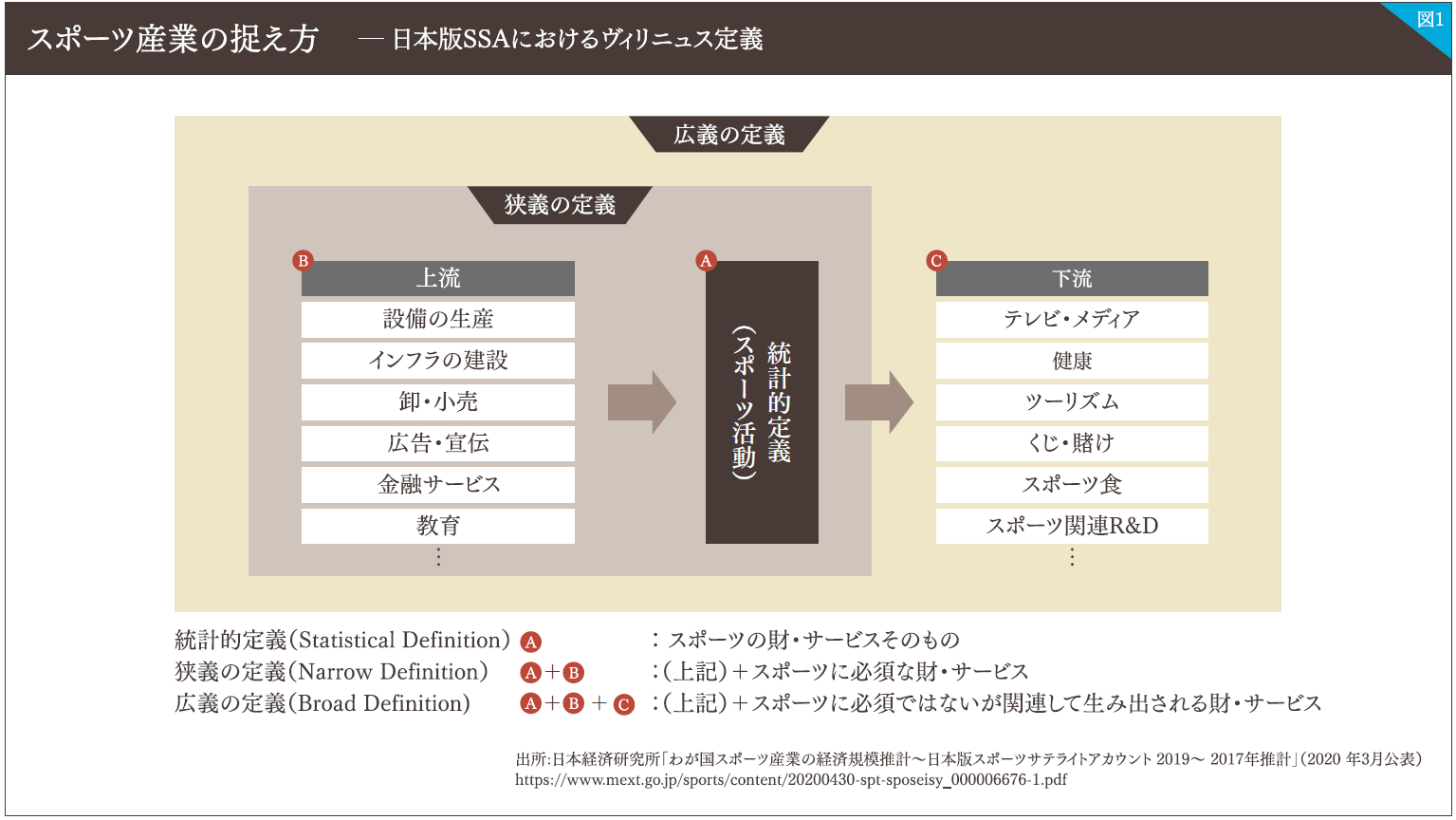

Today, the Japanese version of the Sports Satellite Account (SSA) has been formulated based on the Vilnius definition developed by the European Commission to measure the economic scale of the sports industry, and the components of the sports industry are being expanded (Figure 1).

In the diagram, this corresponds to an expansion of Area C, which includes "goods and services that are not essential to sports but are produced in a related manner." Businesses related to this area are underdeveloped in Japan. The government's expectations for the sports industry are based on the significant potential that lies dormant in this area, which is reflected in the target figure of 15 trillion yen. The government is focusing on promoting the realization of this potential.

In practice,……

To read the full text, please download the PDF.

DownloadPDF(1.51 MB)